Equity investors usually start with one strong belief. Businesses grow over time, and equity represents ownership in those businesses. When companies earn more, their value rises. This logic feels clear and easy to trust. Because of this, most long-term portfolios focus heavily on equity.

Gold feels very different. It does not grow profits. It does not pay dividends. Nothing expands when you hold gold. It simply holds value. Because of this, many equity investors feel gold is inactive or unnecessary, so it slowly gets pushed out of the conversation.

Over time, performance comparison strengthens this belief. Equity has delivered higher returns than gold over long periods. This fact is repeated often and is mostly true. As a result, investors begin to see gold as something that slows progress rather than supports it.

That comparison, however, misses an important point. Equity and gold are not meant to do the same job.

Equity is a growth asset. Its role is to increase wealth over many years. Gold is a stability asset. Its role is to protect value when conditions become uncertain. When both are judged by the same standard, gold always looks weaker. Portfolio allocation, however, is not about choosing one winner. It is about combining assets that behave differently.

Many equity investors are comfortable with market ups and downs. They accept volatility as part of investing. Because of this comfort, safety feels less valuable. Gold is often called a safe asset, so it feels unnecessary to someone who already believes they can handle risk.

During strong market phases, this thinking works well. Equity rises, portfolios grow, and confidence increases. At the same time, gold often moves slowly. It attracts less attention and feels boring.

Trouble appears during difficult phases. Markets do not rise forever. There are periods when equity falls sharply or stays flat for years. During those phases, emotions change. Confidence weakens. Fear increases. This is when gold quietly shows its purpose.

Gold and equity react differently to stress. That difference explains why gold still matters in portfolio allocation.

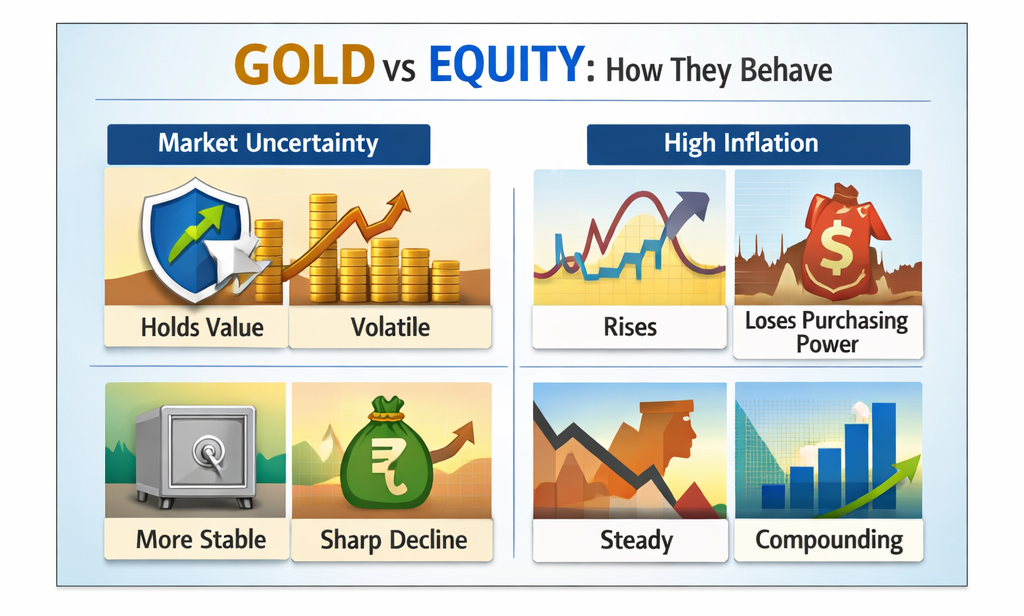

Gold vs Equity: Behaviour in Different Situations

| Situation | Equity | Gold |

|---|---|---|

| Economic growth | Performs strongly | Moves slowly |

| Market uncertainty | Becomes volatile | Often holds value |

| High inflation | Mixed performance | Usually benefits |

| Financial stress | Sharp falls possible | Often more stable |

| Long calm periods | Compounds well | Flat or gradual |

This difference does not make gold better than equity. It makes gold useful in a different way.

Consider a simple example. Two investors each invest ₹20 lakh for the long term. One invests everything in equity. The other invests ₹18 lakh in equity and ₹2 lakh in gold, which is a 10 percent allocation.

When markets rise, the all-equity portfolio may grow faster. When markets fall, the portfolio with gold usually falls less. The difference may look small on paper. Emotionally, it matters a lot.

A portfolio that falls less is easier to stay invested in. Investors who stay calm tend to make fewer mistakes. Over long periods, avoiding mistakes often matters more than chasing the highest return.

This is one reason many experienced investors discuss gold, even if they remain equity focused.

Another reason equity investors ignore gold is perception. Equity feels modern and forward-looking. Gold feels old and traditional. This emotional bias quietly affects decisions.

Gold also does not demand attention. It does not need frequent buying or selling. It does not produce news during calm periods. Because of this, it gets ignored. Ironically, this quiet nature is what makes gold useful.

Recent gold price movements highlight this role. Gold prices tend to rise during periods of inflation concern, currency weakness, or global uncertainty. Central banks across the world have also increased gold purchases to diversify reserves. These factors often support gold prices when confidence in other assets weakens.

For readers interested in how inflation affects assets, you can read this RBI explainer on inflation and purchasing power

https://rbi.org.in/scripts/FAQView.aspx?Id=99

Gold does not need a large allocation. It is not meant to replace equity. Most long-term portfolios that include gold use small ranges, often 5 to 15 percent.

For example, in a ₹10 lakh portfolio:

- 5% gold = ₹50,000

- 10% gold = ₹1,00,000

- 15% gold = ₹1,50,000

This portion is not meant to beat equity. It is meant to behave differently when equity struggles.

If you are new to portfolio thinking, you may also find it helpful to read our article on

“How to Think About Long-Term Investing”

https://waradefinblog.blog/how-to-think-about-long-term-investing/

Gold is not an alternative to equity. It is not a competitor. It is a supporting asset. Equity drives growth over time. Gold helps manage stress during uncertain phases.

Portfolio allocation is not about predicting which asset will perform best next. It is about building a structure that can survive different market conditions.

When seen this way, gold stops looking boring. It also stops being overhyped. It simply takes its place quietly, supporting the portfolio when needed and staying in the background when not.

That is why gold deserves a place in portfolio discussions, even for equity-focused investors.

Pingback: India Budget 2026 Explained: Important Highlights and Impact on Investments